From setting up your company’s eTax account to managing CIT, VAT, and PIT obligations, here is a practical guide for business owners and operators in Vietnam. (This article was originally published on 1 May 2026 on our Substack)

Running a business in Vietnam means navigating a set of recurring tax obligations that do not pause between quarters. Corporate income tax, value added tax, personal income tax withheld from employees, electronic invoicing, and annual finalization are all expected to flow through the eTax system, the GDT’s central digital platform for tax compliance. The stakes for staying connected are real: if your company’s eTax account goes offline, your filing workflow stops entirely, and the penalties for missing deadlines compound quickly.

This guide covers what business owners need to know: the portals, your tax code, the taxes you owe, key deadlines, how to set up your eTax account, and what the penalties look like if something slips.

The eTax System for Businesses: Portals and Access

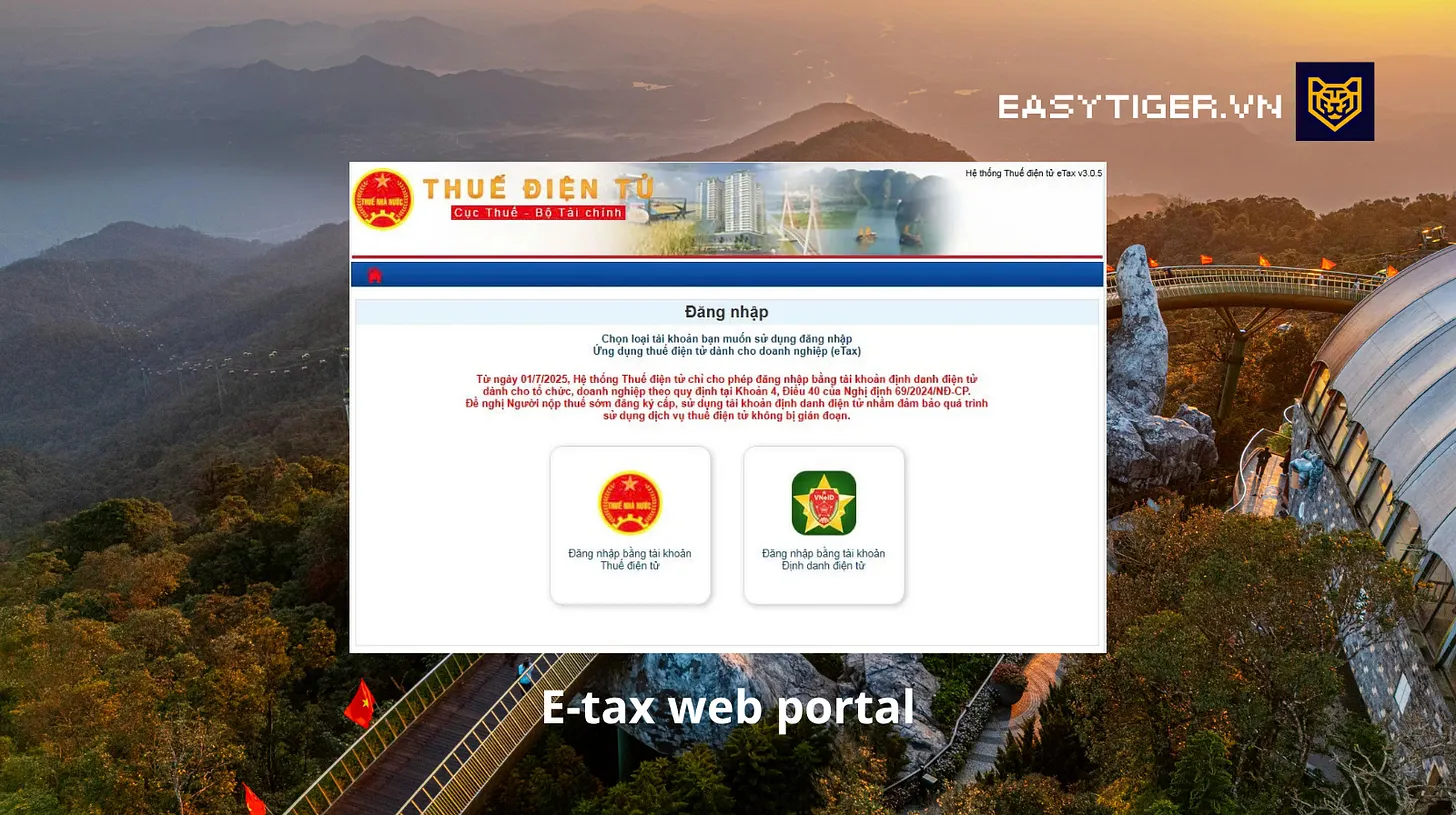

The main business eTax portal at thuedientu.gdt.gov.vn is the full-feature platform for organizations. It handles tax registration, periodic declaration filing, online payment, document submission, and status tracking. This is where your accountant or tax agent will spend time during monthly and quarterly filing cycles, as well as during the annual finalization push in March.

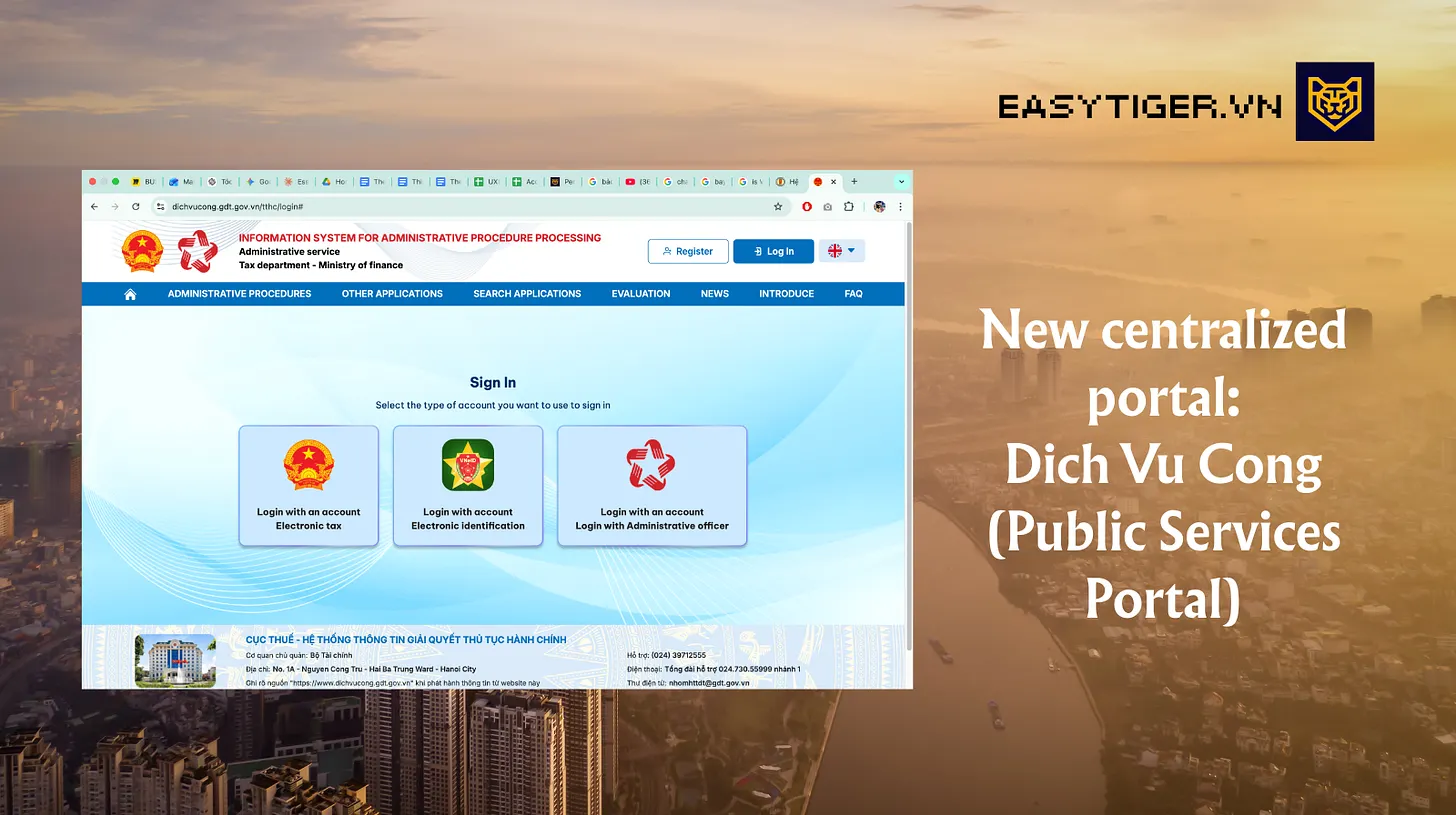

The GDT has also been rolling out a centralized administrative portal at dichvucong.gdt.gov.vn, which handles a broader scope of procedures beyond standard tax filings, including certain business-related administrative declarations. This portal is accessible to both individuals and businesses via a VNeID-linked account or username-and-password credentials.

On the eTax web portal, businesses can log in using two methods: either through the company’s existing eTax credentials (username and password) or, through a linked VNeID organizational account authenticated by the legal representative or an authorized person. The VNeID login is now the recommended route, as it ties access to biometric-verified identity and eliminates the risk of credential loss that caused so many headaches under the old password-only system.

On the eTax Mobile app, the legal representative cannot access the company’s eTax account directly as a business entity. However, if the business VNeID account is properly linked, the company’s tax filings and submission records appear alongside the legal representative’s personal tax information within the same session. This means you can keep an eye on your company’s pending declarations and your own PIT obligations in one place, without logging in and out between accounts.

For businesses engaging with foreign digital or service providers, there is also a dedicated portal at etaxvn.gdt.gov.vn for foreign suppliers and cross-border digital platforms. Foreign entities without a registered presence in Vietnam can register, declare, and pay taxes through this channel remotely.

Your Company’s Tax Code

When you register a company in Vietnam, the business registration code on your Business Registration Certificate (GCN), issued by the Department of Planning and Investment, is automatically your tax code. No separate tax registration is required.

However, having a tax code and being able to actively transact on the eTax system are two different things. To file returns, make quarterly and monthly tax payments, and interact electronically with the GDT, your company needs a verified electronic transaction account (eTax account) on the eTax portal. This requires a valid digital signature (USB token hardware or an approved cloud-based digital signature) registered with the GDT, alongside the corresponding signing software installed on the filing machine.

All of these steps form a standard post-incorporation checklist that a dedicated accounting or company formation service can handle on your behalf, which is how most newly established businesses in Vietnam approach this.

When Does a Business Start Paying Tax?

All companies registered in Vietnam, including foreign-invested enterprises and single-member LLCs, are subject to Corporate Income Tax, Value Added Tax, and are required to withhold and remit Personal Income Tax for their employees. These obligations begin from the moment the company issues its first taxable invoice or generates taxable revenue. There is no grace period.

Businesses are also required to file periodic declarations even in months or quarters when revenue is zero or tax owed is zero. A nil return is still a required return. Silence is not the same as compliance.

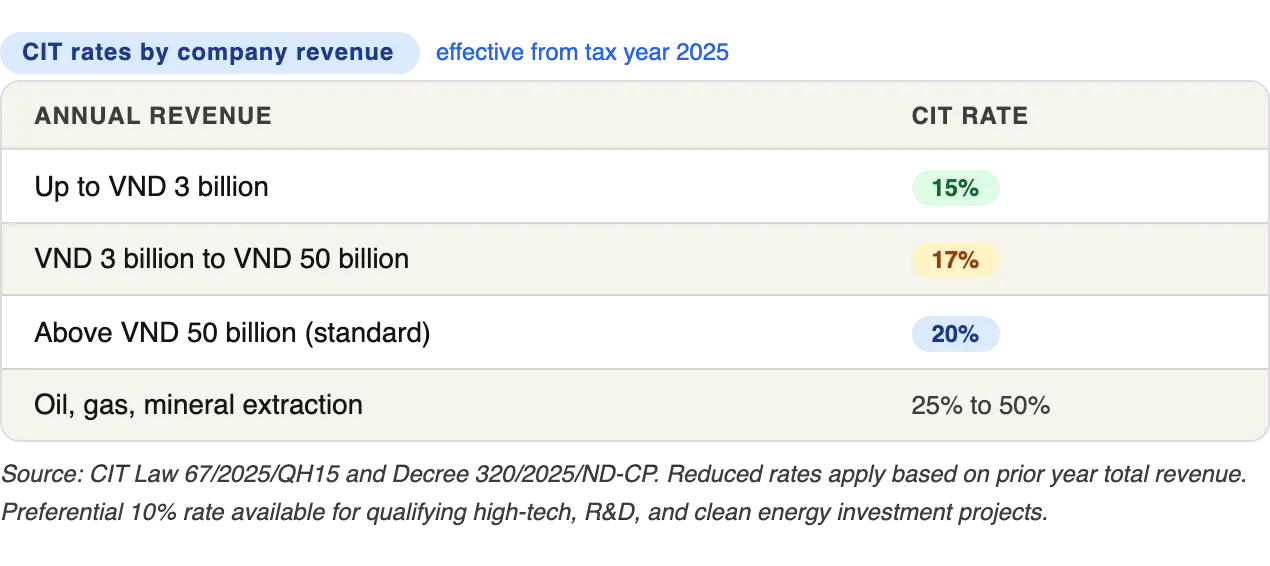

Corporate Income Tax (CIT)

The standard CIT rate is 20% of taxable profit. Under the new CIT Law 67/2025/QH15, effective from October 1, 2025 and applying from the 2025 tax year, reduced rates are now available for small and micro enterprises based on annual revenue.

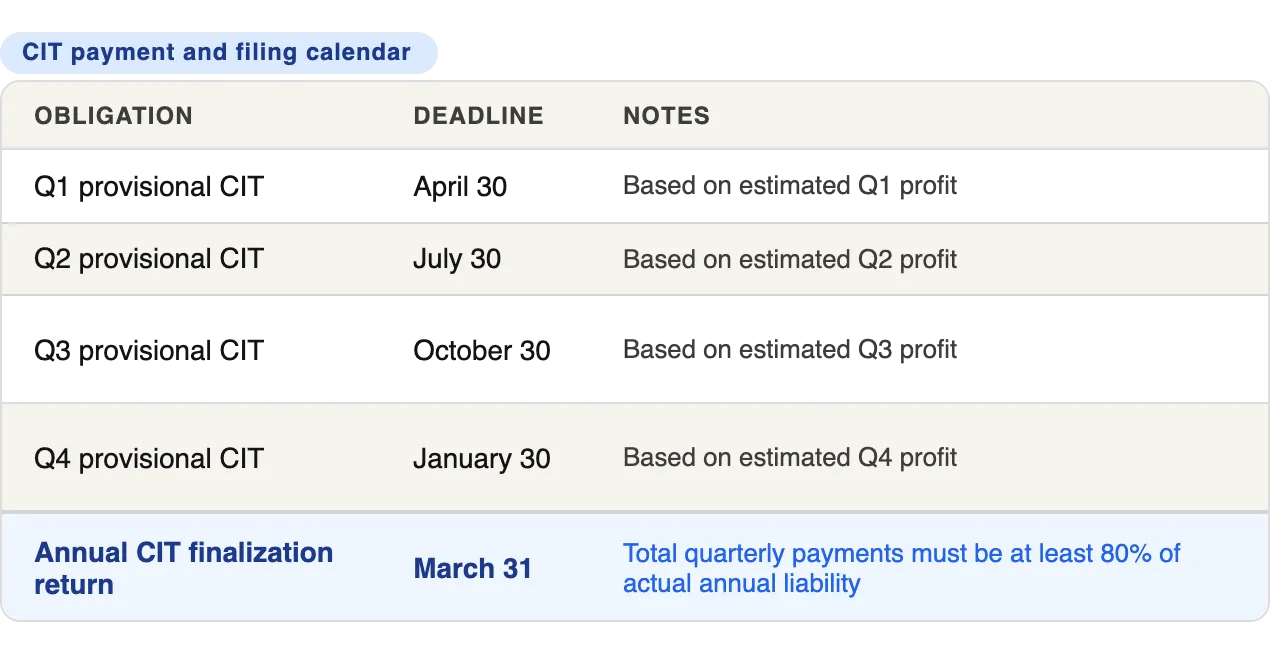

Quarterly Payments and Annual Finalization

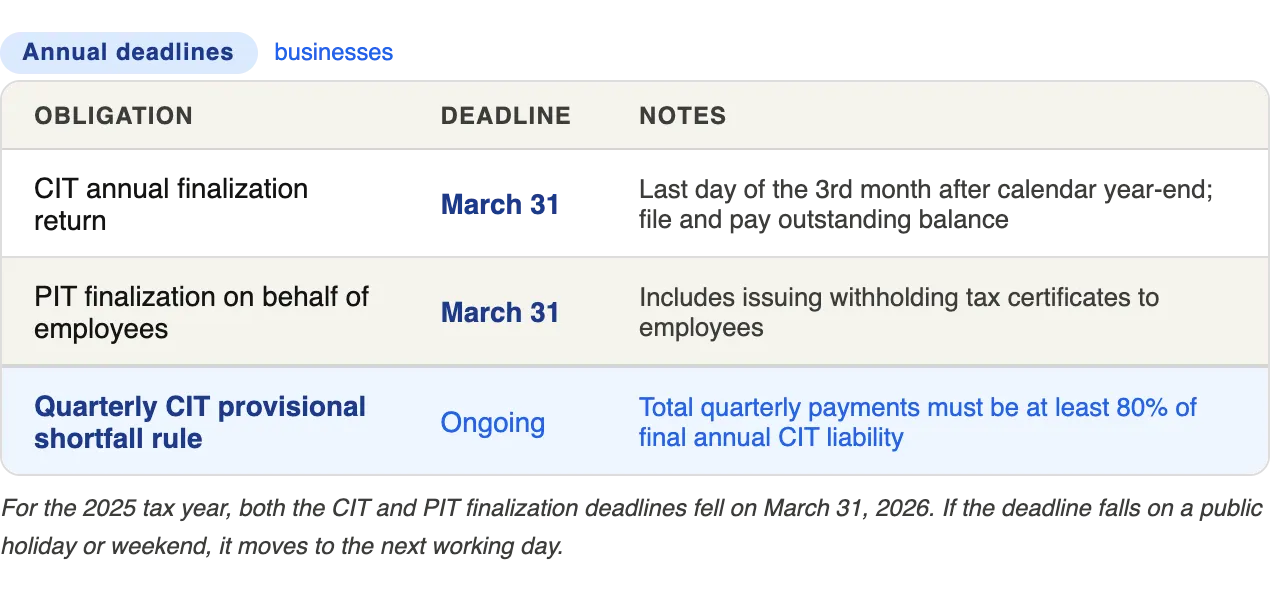

Businesses make provisional CIT payments quarterly, no later than the 30th day of the month following each quarter. The annual CIT finalization return is due by March 31 of the following year. One rule that catches many companies off-guard: total provisional quarterly payments must cover at least 80% of the final annual tax liability. If they fall short, late payment interest at 0.03% per day accrues on the shortfall from the date those payments were due.

For a UX Design company like ours, the quarterly cycle involves declaring provisional CIT, declaring VAT, and remitting PIT withheld from employee salaries, all through the eTax web portal. Each quarter, the accountant compiles declarations, signs digitally, and submits. Annual finalization in March reconciles the full year’s result against provisional payments.

Value Added Tax (VAT)

The standard VAT rate is 10%, with a temporary 2% reduction extended through December 31, 2026, bringing the effective rate to 8% for most goods and services. Notable exceptions where the full 10% continues to apply include telecommunications, financial services, banking, securities, insurance, real estate, metal products, and extractive industries (excluding coal). Exports are taxed at 0%.

Most small and medium businesses file quarterly. The VAT deduction method applies to companies that issue VAT invoices. Businesses whose annual revenue is below VND 200 million are exempt from VAT obligations starting from 2026 under the new VAT Law 48/2024/QH15, up from the previous threshold of VND 100 million.

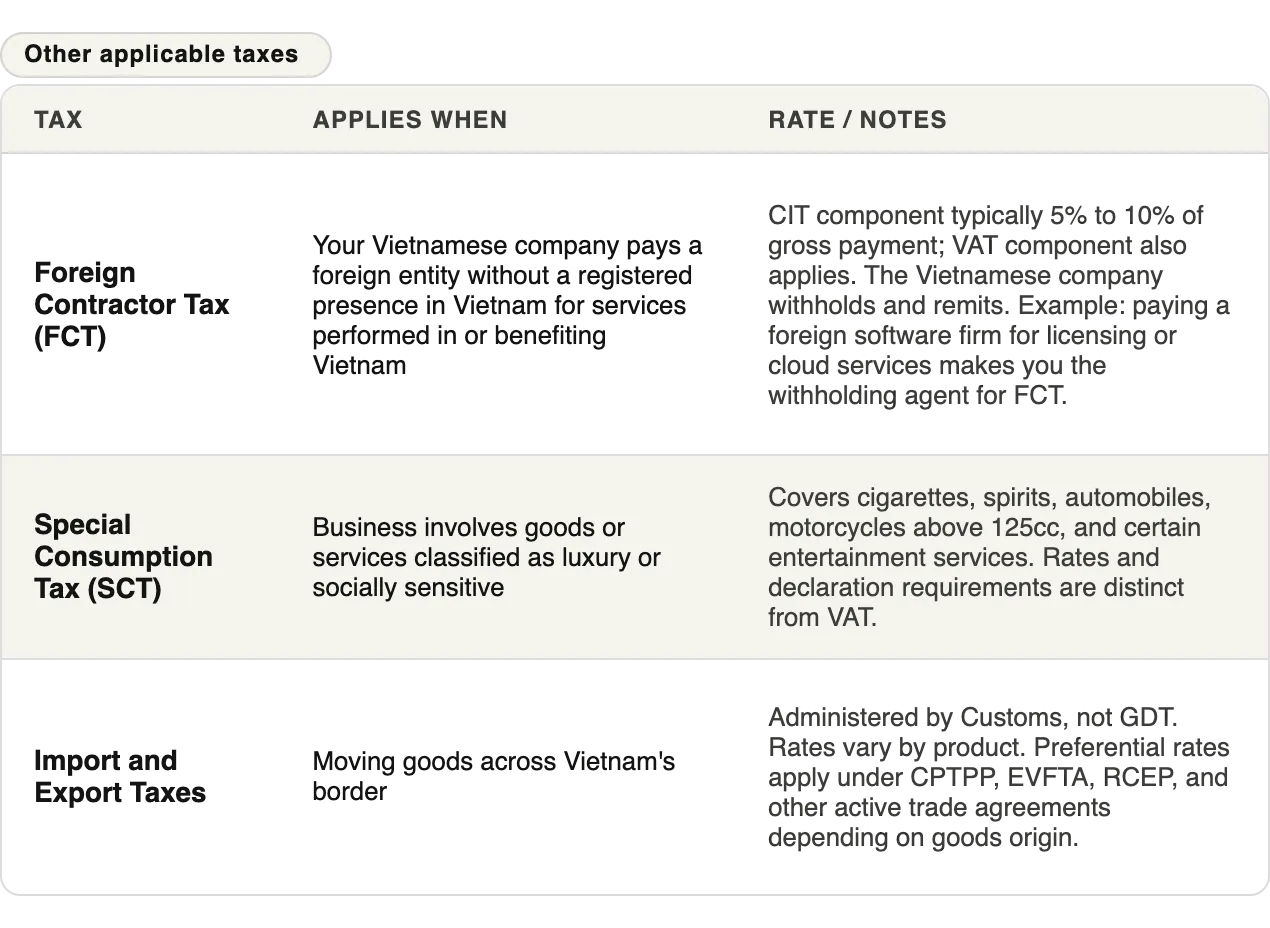

Other Taxes Businesses Need to Know

Registering and Setting Up Your Business eTax Account

Obtaining your tax code from the Business Registration Certificate is step one, but it is only the beginning. To file and pay taxes electronically, your company needs an active eTax transaction account with a working digital signature. Before you begin, your company must meet five conditions: it must be an active registered entity with a valid tax code, hold a valid digital certificate from a licensed CA provider, have a stable internet connection and email address, be actively filing tax declarations, and have at least one registered business bank account.

Step 1: Obtain a valid digital signature (chu ky so)

Before anything else on the eTax portal can be completed, your company needs a valid digital signature. This is either a USB token (hardware key issued by a licensed CA provider such as VNPT-CA, Viettel-CA, MISA eSign, or NewCA) or an approved remote cloud-based digital signature. The USB token is plugged into the signing computer when authenticating and submitting declarations. The cloud-based option, increasingly common, uses a mobile app and PIN confirmation in place of physical hardware. Without a registered, active digital signature, you cannot create an eTax account or sign any official tax declarations.

Step 2: Register your eTax transaction account

There are two routes:

- Via thuedientu.gdt.gov.vn: Go to the business section, click Register, enter your company’s tax code, and fill in the required fields including the legal representative’s name, phone, email, and digital signature details. Link your business bank account at this stage for future tax payments. After completing the form and signing digitally with your USB token or cloud signature, submit the registration declaration (Form 01/DK-TDT). The GDT reviews and activates the account, after which you can begin filing.

- Via dichvucong.gdt.gov.vn (recommended for new registrations): Log in using your VNeID organizational account. The portal guides you through the same registration steps but with real-time status tracking and OTP confirmation, which makes troubleshooting significantly easier than the older standalone portal.

Step 3: Register for electronic invoicing (Hoa Don Dien Tu)

Once your eTax account is active, register for e-invoicing through the GDT portal. This is mandatory for all businesses in Vietnam. E-invoices must be issued in standardized XML format and transmitted to the GDT for real-time validation. You will need to select an e-invoice service provider, configure your invoice template, and complete the registration form on the portal before issuing your first invoice.

Step 4: Link the corporate VNeID account

To use VNeID login on the eTax portal and authorize your accountant to file on the company’s behalf, the legal representative must register the company’s organizational VNeID account. This is done through the VNeID mobile application using the legal representative’s personal Level 2 VNeID, or by submitting Form TK02 in person at the local Citizen Identification Management Agency (Cong an). Once the corporate VNeID is active, the legal representative can delegate tax filing authority to an accountant through the portal’s authorization function, without handing over master credentials.

HTKK software: Many companies also use HTKK, the GDT’s free offline declaration tool, to prepare complex returns before uploading and signing them via the eTax web portal. This is especially common for quarterly CIT provisional declarations and the annual finalization return, where the software handles bracket calculations and form generation before the accountant signs and submits online.

Paying Tax Online

Once your eTax account is active, tax payments flow through the portal’s payment section or directly through your business bank. Most major Vietnamese banks, including Vietcombank, Techcombank, BIDV, and foreign banks like Shinhan, support eTax payment integration. The process generates a unique payment reference code, which you enter through your bank’s internet banking or mobile banking, and the GDT records the payment against your outstanding obligation in real time.

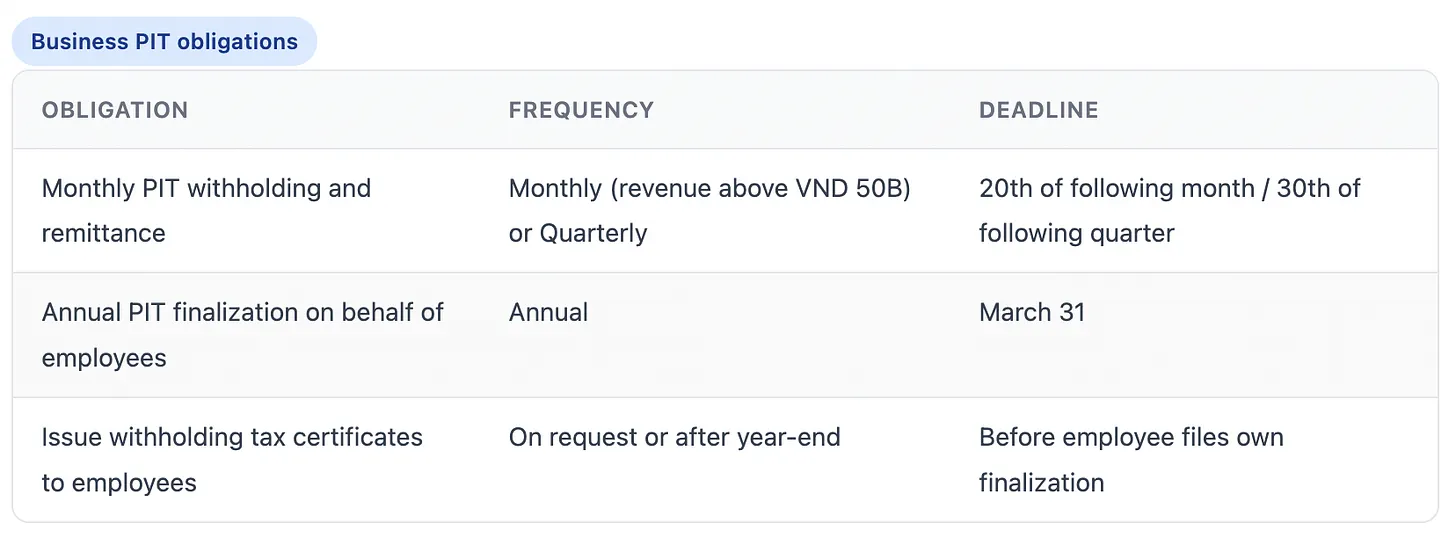

PIT Obligations for Businesses: Withholding, Calculation, and Finalization

As a business with employees, you are responsible for withholding PIT from employee salaries each month, remitting it to the GDT, and filing annual PIT finalization on behalf of your staff by March 31.

Business PIT obligations

Employees who had only one employer for the full year and are still employed may authorize the company to file their PIT finalization. Employees with multiple income sources, or those who left before year-end, must file their own finalization directly with the GDT.

Tax Finalization Deadlines

For the 2025 tax year, the CIT and PIT finalization deadline was March 31, 2026. The finalization cycle involves reconciling provisional quarterly CIT payments against the actual annual taxable profit, then filing the final return and settling any remaining balance.

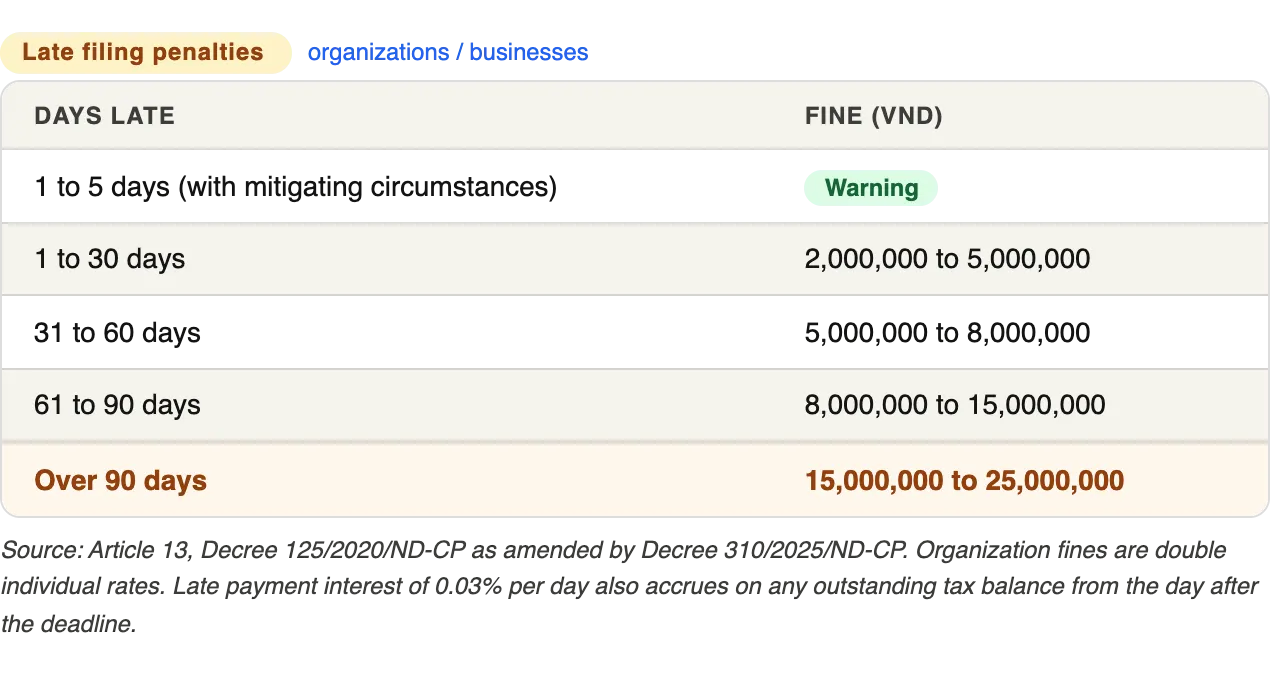

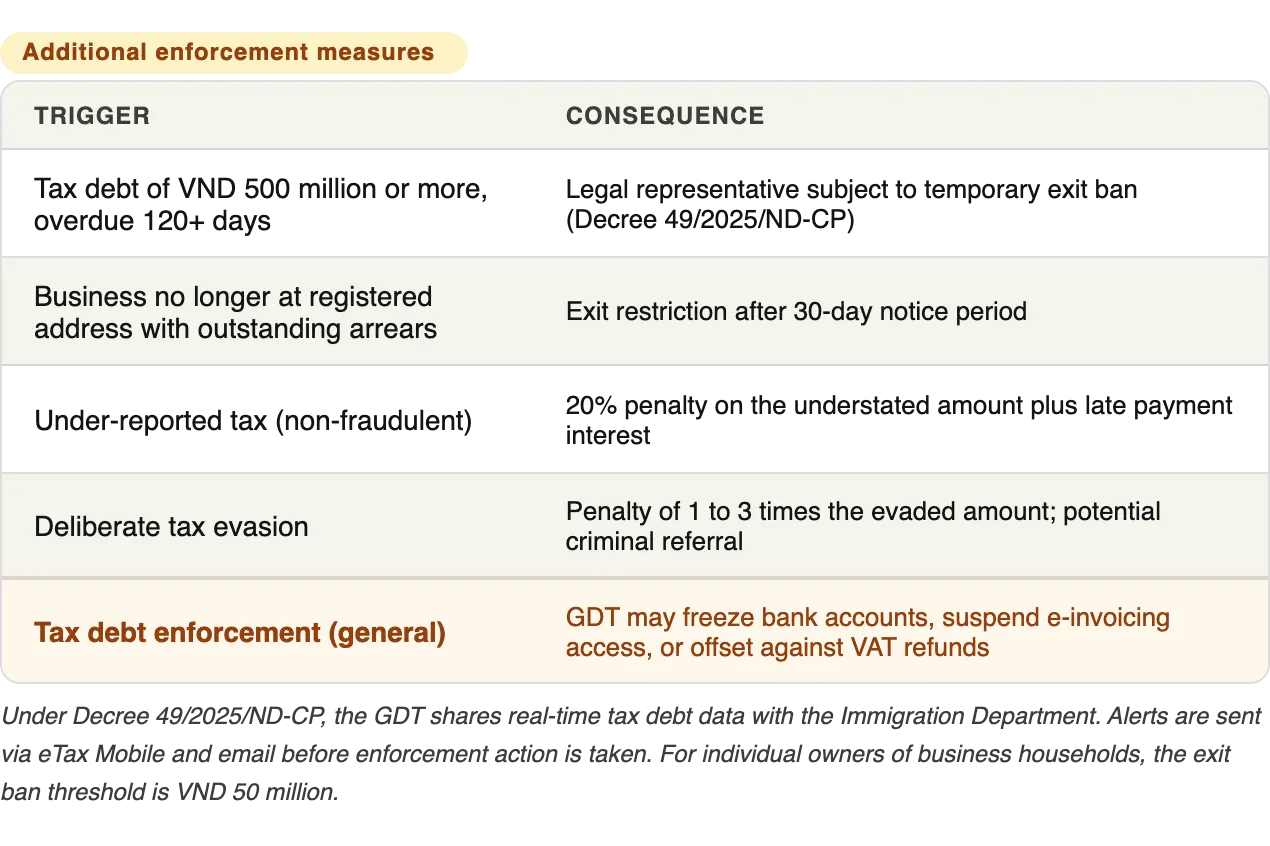

Penalties for Late Filing

The same penalty framework applies across PIT, CIT, and VAT filings. Under Decree 125/2020/ND-CP as amended by Decree 310/2025/ND-CP, penalties for organizations are double those for individuals filing the same type of return late. Late payment interest of 0.03% per day applies separately to any outstanding tax balance, running from the day after the deadline continuously until payment is made.

Closing Note

Running a business in Vietnam’s tax environment in 2026 requires active attention. The CIT rate changes, quarterly provisional rules, VAT stimulus measures, e-invoicing requirements, and the VNeID transition all landed within a short window. Staying on top of them is not just a compliance exercise. It is how you avoid penalties that can easily outpace the underlying tax owed.

The eTax system itself has improved. VNeID single sign-on removed the most painful login friction. The Dich Vu Cong portal added transparency to document processing. Electronic payments with major banks work reliably. What still takes effort is knowing what to file, when to file it, and how to structure your quarterly provisionals to avoid the 80% shortfall trap at finalization.

If you need support setting up your company’s eTax account, managing quarterly filings, handling FCT for foreign contractor payments, or navigating the annual finalization process, reach out to EasyTiger and we will connect you with a verified accounting or tax specialist who works with businesses in Vietnam regularly.

This article is for informational purposes only and does not constitute formal tax or legal advice. Tax regulations in Vietnam are subject to ongoing changes. All rates, thresholds, and deadlines referenced are based on information available as of April 2026. Consult a qualified tax professional for guidance specific to your situation.